Then, you can look at your accounts to get a snapshot of your company’s financial health. That happens when you move the temporary account balances at the end of the year into a permanent account. We will help you understand how temporary accounts work, why we must close them at the end of the year, and where the money in them goes. Permanent accounts are defined as accounts that remain open accounts throughout a business period.

Accounting is one of the most complex areas of business management. Among its many complexities are the accounts used for categorizing the flow of money. Most business owners are familiar with the core account types, such as revenue and expenses.

Temporary accounts

In a business, there are many different types of accounts that can be used to manage finances. The definition of a temporary account is an account whose balance is not carried over at the end of every accounting year and thus begins the new year with zero balance. The primary use of a temporary account is to show how any draws, expenses, and/or revenue have affected an equity account. These accounts track business expenses and revenue to calculate the net loss and net profit for a specific period.

Permanent accounts are asset accounts, liabilities, and equity accounts you’ll see on the balance sheet. Revenue refers to the total amount of money earned by a company, and the account needs to be closed out at the end of the accounting year. To close the revenue account, the accountant creates a debit entry for the entire revenue balance.

By closing these accounts after a specified period, the business can separate financial data into periods that provide a clearer picture of its financial performance. This article will compare permanent and temporary accounts to help you better understand the critical differences between the two to better manage them in the future. Your accounts help you sort and track your business transactions. Each time you make a purchase or sale, you need to record the transaction using the correct account.

What is the Difference Between Permanent and Temporary Accounts?

Any balances remaining in those accounts are transferred to a permanent account. Accountants then prepare financial documents to show that this took place. When the next fiscal period starts, the new account begins at zero. Financial management accounts can consist of assets, expenses, liability, equity, and revenue, all of which can be grouped into permanent and temporary accounts. Either way, you must make sure your temporary accounts track funds over the same period of time.

- Permanent accounts always maintain a balance and start the next period out with the ending balance from the prior period.

- Permanent accounts are the accounts that are seen on the company’s balance sheet and represent the actual worth of the company at a specific point in time.

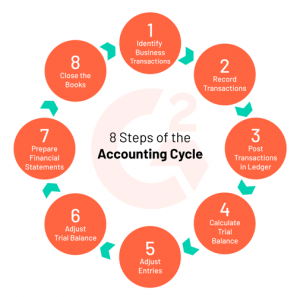

- These are called closing entries, and they reset the balances and close the temporary accounts for the year to prepare them for the new accounting cycle.

- Otherwise, these funds will create a discrepancy in the general ledger, resulting in miscalculations across other accounts.

Closing entries are taught in accounting classes to help students understand the accounting process and how financial information moves through the accounting software. A business may be a sole proprietorship, partnership or a corporation but the accounts under Capital are all considered as permanent accounts just the same. It is for this reason that accountants also review the need of new permanent accounts or whether or not some permanent accounts need to be combined. For example, suppose a company sets aside a certain percentage of earnings in a temporary account for quarterly taxes. The remaining balance must then be redistributed at the end of the quarter to avoid discrepancies in the general ledger. Permanent accounts differ from temporary accounts as they are, as their name suggests, designed for long-term savings and investment goals rather than short-term initiatives.

The importance of understanding the distinction between financial accounts

One of the most crucial aspects of corporate management is accounting. It involves recording and maintaining transaction details for different accounts. Guest faculty and staff, visiting scholars and others may receive temporary computing privileges when deemed necessary by an affiliated UC Davis department. Temporary accounts are active for a maximum of one (1) year, or until the owner’s affiliation with UC Davis ends, whichever comes first. Renewal of this account is required for continuation of services beyond one (1) year.

At the end of the accounting period, those balances are transferred to either the owner’s capital account or the retained earnings account. Which account the balances are transferred to depends on the type of business that is operated. Permanent accounts are the accounts that are seen on the company’s balance sheet and represent the actual worth of the company at a specific point in time.

What is a Permanent Account?

Whether you run a small business or a large corporation, it’s helpful to understand the different types of accounts used in the accounting process. With a fully automated accounts receivable operation, you can streamline this process, reduce the risk of derailing your company’s financials, and enhance your overall success. Understanding your business’s equity accounts is essential because they provide a clear picture of who has a stake in the company and how much they have invested.

The purpose of temporary accounts is to show how any revenues, expenses, or withdrawals (which are usually called draws) have affected the owner’s equity accounts. The accounts that fall into the temporary account classification are revenue, expense, and drawing accounts. The meaning of permanent accounts are accounts whose balances remain open at the definition and formula of social security tax the end of the accounting time and are carried over to the next accounting period. The balance at the end of an accounting period becomes the beginning balance for the next period, and is viewed on the company or individual’s balance sheets. Permanent accounts represent the worth of a company at a specific time and are also called real accounts.

Temporary accounts are reset to zero by transferring their balances to permanent accounts. Starting an accounting period with a zero balance enables businesses to monitor activity for a specific accounting period without mixing up data from two different time periods. There is no predetermined fiscal period to maintain a temporary account, but it usually lasts for a year or less. Quarterly temporary accounts are fairly common, especially when it comes to tax payments or measuring the company’s financial performance. In fact, these accounts make it easier for businesses to track the achievement of milestones.

One of the main differences between balance sheets and income statements is that a balance sheet includes permanent accounts, while an income statement includes temporary accounts. Unlike temporary accounts, you do not need to worry about closing out permanent accounts at the end of the period. Instead, your permanent accounts will track funds for multiple fiscal periods from year to year.

The accountant then needs to make a debit of $5,000 from the drawings account and a credit of the same amount to the capital account. Normally these balances represent Revenues (income, gains, services) and Liabilities (salaries, providers, credits). Permanent accounts tell you exactly what you own or owe right now. That’s because it shows you how much goods you have at the moment, instead of over a certain month, year, a few years, or any other specific amount of time.

Cash Management Software

Then, another $200,000 worth of revenues was seen in 2017, as well as $400,000 in 2018. If the temporary account was not closed, the total revenues seen would be $900,000. Temporary accounts are in the grouping of income statement accounts. Below is a list of temporary accounts and a detailed explanation of their meaning.

How to Get Past Paywalls: Read Paid Articles for Free – TechPP

How to Get Past Paywalls: Read Paid Articles for Free.

Posted: Fri, 14 Jul 2023 07:00:00 GMT [source]

After the other two accounts are closed, the net income is reflected. Taking the example above, total revenues of $20,000 minus total expenses of $5,000 gives a net income of $15,000 as reflected in the income summary. Permanent accounts (also called real accounts) are those ledger accounts whose closing balance in one period becomes their opening balance in the next period. With a temporary account, the balance gets reset each time you start a new accounting period. In contrast, permanent account balances carry over, meaning the ending balance of a permanent account becomes the starting balance for the next period.