Use of a checklist with deadlines in the accounting cycle improves accountability and process management. Permanent accounts are accounts that continue to accumulate balances across multiple accounting periods. They include asset, liability, and equity accounts, such as Cash, Accounts Receivable, Accounts Payable, and Common Stock.

Post Closing Journal Entries To Close the Books

The accounting cycle is a methodical set of rules that can help ensure the accuracy and conformity of financial statements. Computerized accounting systems and the uniform process of the accounting cycle have helped to reduce mathematical errors. The software auto-generates financial statements so you can directly close your books at the end of the reporting period.

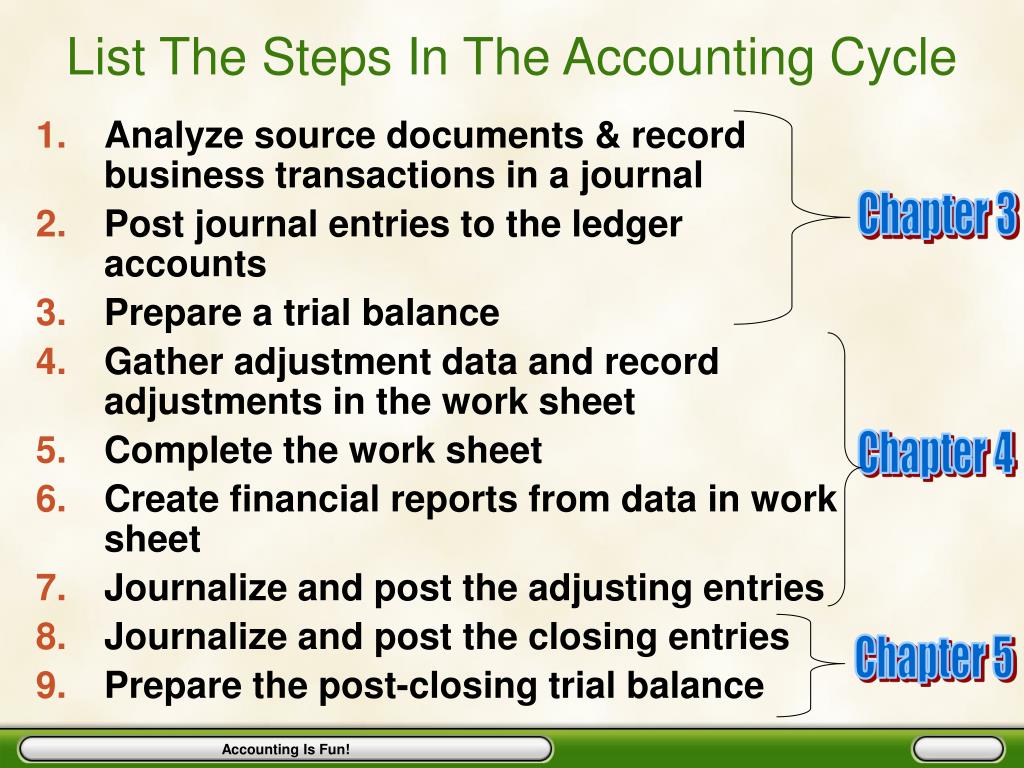

The 9-step accounting process

Closing entries are journal entries made to transfer the balances of these temporary accounts to a permanent account, usually the Retained Earnings account. This helps to update the Retained Earnings account balance to match the end-of-period balance. While posting, each journal entry is dissected according to its debit and credit components, which are then assigned to their respective ledger accounts. At the start of the next accounting period, occasionally reversing journal entries are made to cancel out the accrual entries made in the previous period. After the reversing entries are posted, the accounting cycle starts all over again with the occurrence of a new business transaction. The main difference between the accounting cycle and the budget cycle is that the accounting cycle compiles and evaluates transactions after they have occurred.

Step 3: Post Transactions to the General Ledger

From time to time, you may hear it referred to as the bookkeeping cycle. The trial balance gives you an idea of each account’s unadjusted balance. Such balances are then carried forward to the next step for testing and analysis. The purpose of an unadjusted trial balance is to ensure that the total debits equal the total credits, identifying any potential computational errors throughout the first three steps in the cycle.

Best (Vendor-Specific) Accounting Software Training Programs

The closing step impacts only temporary accounts, which include revenue, expense, and dividend accounts. The permanent or real accounts are not closed; rather, their balances are carried forward to the next financial period. Closing the books at the end of an accounting cycle involves closing temporary accounts, such as revenues, expenses, and dividends (or withdrawal) accounts. These accounts are referred to as temporary because their balances are reset to zero at the end of each cycle. This is crucial to provide accurate financial statements and ensure that the company’s accounts accurately reflect its financial position. According to the rules of double-entry accounting, all of a company’s credits must equal the total debits.

- It comprises a series of eight steps that deal with the recording, analysis, and reporting of financial transactions.

- After closing, the accounting cycle starts over again from the beginning with a new reporting period.

- Accounting is made up of all of the ways that a business’s money moves.

- This means your books are up to date for the accounting period, and it signifies the start of the next accounting cycle.

- Cash accounting requires transactions to be recorded when cash is either received or paid.

Run your business with confidence

Learn the eight steps in the accounting cycle process to complete your company’s bookkeeping tasks accurately and manage your finances better. Adjusting entries are made at the end of an accounting period to adjust those accounts that need to be updated or adjusted. Adjustments include the recording of depreciation expense, the gradual release of prepayments, and the recording of bookkeeping and accounting task checklist earned revenue from unearned revenues at the end. Temporary or nominal accounts, i.e. income statement accounts, are closed to prepare the system for the next accounting period. These items are measured periodically, hence need to be closed to have a “fresh slate” for the next accounting period. Business transactions are usually recorded using the double-entry bookkeeping system.

At the end of any accounting period, a trial balance is calculated for all accounts on the general ledger. This trial balance tells the company the amount of cash each unadjusted account is worth. Calculating these balances is crucial, as they are used for testing and analysis. This is the point in the cycle where the method of accounting has to be chosen.

The general ledger accounts utilize double-entry bookkeeping, which is an essential principle in accounting. Double-entry bookkeeping states that for every transaction, there must be a debit entry and a credit entry. This ensures that the accounting equation is balanced and that assets are always equal to liabilities plus equity. Obviously, business transactions occur and numerous journal entries are recording during one period. Preparing a worksheet involves aggregating the debits and credits made during the current accounting period into a spreadsheet. If the debits and credits don’t match, you’ll need to make the necessary adjusting entries to prepare the adjusted trial balance.